In the mid- to late-1990s several books were written about accounting in the lean enterprise (companies implementing elements of the Toyota Production System). These books contest that traditional accounting methods are better suited for mass production and do not support or measure good business practices in just-in-time manufacturing and services. The movement reached a tipping point during the 2005 Lean Accounting Summit in Dearborn, Michigan, United States. 320 individuals attended and discussed the advantages of a new approach to accounting in the lean enterprise. 520 individuals attended the 2nd annual conference in 2006 and it has varied between 250 and 600 attendees since that time.

If you are relying on your education to meet qualification requirements:

Marginal costing (sometimes called cost-volume-profit analysis) is the impact on the cost of a product by adding one additional unit into production. The contribution margin of a specific product is its impact on the overall profit of the company. Margin analysis flows into break-even analysis, which involves calculating the contribution margin on the sales mix to determine the unit volume at which the business’s gross sales equals total expenses.

How can online courses help me learn management accounting?

Management accountants will work as part of a team to produce budgets and forecasts, while monitoring and reporting the overall performance of a business. The work of management accountants will often be used by board-level executives and strategists to make key decisions. In addition, management accountants can also highlight trends that offer useful insights to help plan for the future.

Management Accounting Degree Concentration

- Most companies record their financial information on the accrual basis of accounting.

- Companies that fail to demonstrate a credible commitment to transparency and sound ESG practices may encounter difficulties in accessing external financing, attracting skilled labor, gaining community acceptance, or maintaining societal legitimacy.

- Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us.

- They don’t need to adhere to GAAP since the ad-hoc reports are informal and for internal use only.

- A poorly structured selling and administrative expense budget can affect not just tactics but also strategy.

- This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible.

Mismanaging restricted funds can result in serious consequences for nonprofits, from legal challenges to diminished donor trust. By being aware of common pitfalls and implementing preventive strategies, nonprofits can protect their reputation and maintain donor confidence. The decision whether or not to cooperate with other universities or research groups depends on future project choices.

Cost-Volume-Profit (CVP) Analysis

The results of an annual survey found that organizations have made minimal gains in risk oversight over the past five years despite an increasingly threatening risk landscape. Most senior executives are pleased by the impact of moving their supply chains closer to home, according to a KPMG report. The path to becoming a managerial accountant isn’t easy, but it’s well worth the effort. GAAP — or Generally Accepted Accounting Principals — are a set of standards that govern corporate accounting. Managerial accountants are the closest a company can get to hiring a fortune teller. Part 2 of the CMA exam covers professional ethics, and all CMAs must complete annual ethics training as a part of their continuing professional education, or CPE requirements.

How Managerial Accounting Works

The Big 4 accounting firm announced that it will invest $1 billion over three years in talent and technology. Finance decision-makers in a quarterly survey say they have concerns on several fronts. As a result, business and industry executives have lower revenue and profit projections. Managerial accounting does not have to adhere to GAAP so long as the ad-hoc reports are for internal use only, and not official.

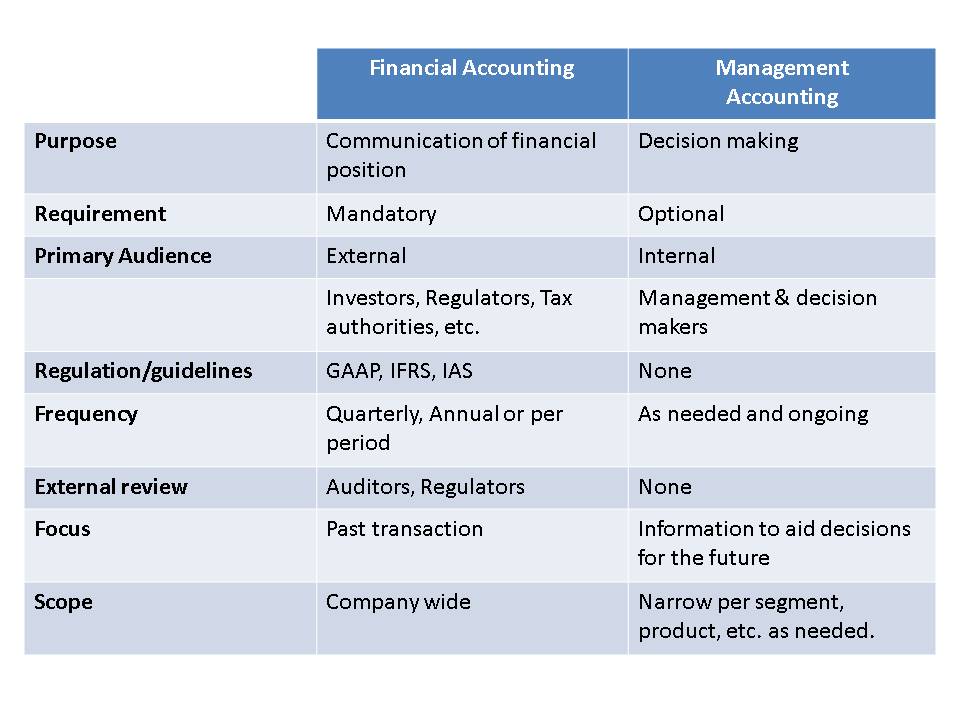

Managers need to know what is happening in their organization when it comes to sales, costs, assets, liabilities, and profitability. For example, if a manager is interested in making decisions concerning inventory levels in several parts of the business, Management Accounting information is needed. While they often perform similar tasks, financial accounting is the process of preparing and presenting official quarterly or annual financial information for external use. Such reports may include audited financial statements that help investors and analysts decide whether to buy or sell shares of the company. Resource consumption accounting (RCA) is formally defined as a dynamic, fully integrated, principle-based, and comprehensive management accounting approach that provides managers with decision support information for enterprise optimization. RCA emerged as a management accounting approach around 2000 and was subsequently developed at CAM-I,[20] the Consortium for Advanced Manufacturing–International, in a Cost Management Section RCA interest group[21] in December 2001.

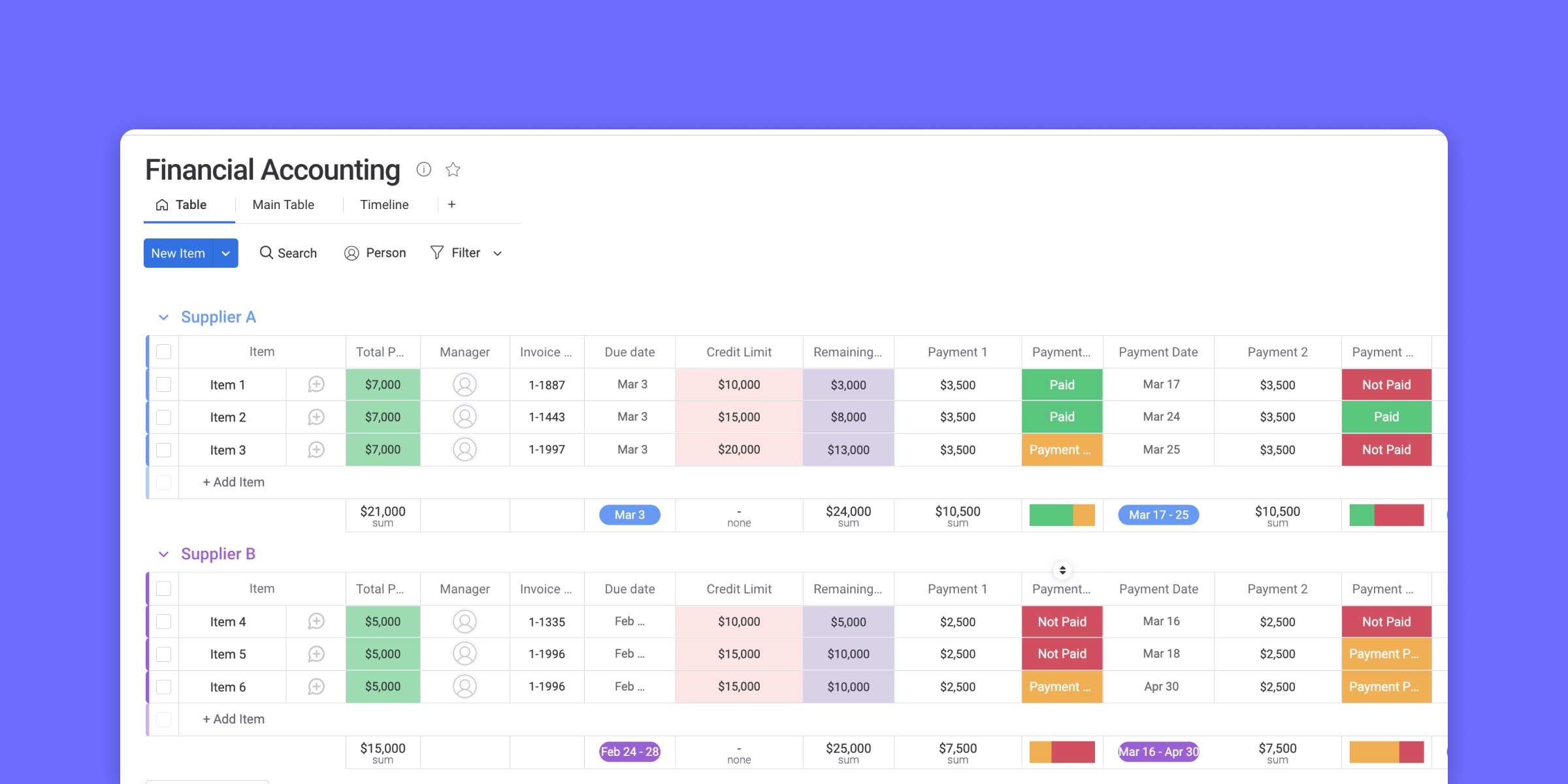

Managerial accountants perform cash flow analysis in order to determine the cash impact of business decisions. Most companies record their financial information on the accrual basis of accounting. Although accrual accounting provides a more accurate picture of a company’s true financial position, it also makes it harder to see the true cash impact of a single financial transaction. A managerial accountant may implement working capital management strategies in order to optimize cash flow and ensure the company has enough liquid assets to cover short-term obligations. The information gathered and summarized for these internal groups is customized to provide feedback for planning, decision making, and evaluation purposes. Managerial reports do not necessarily follow any particular format, but instead are uniquely designed to meet the needs of specific users.

Financial accounting involves producing periodic reports called financial statements to inform such external groups as investors, boards of directors, creditors, and government/tax agencies about a company’s financial performance and status. The income statement, retained earnings statement, balance sheet, and statement of cash items that make up merchandise inventory flows are published at fixed intervals to summarize the historical earnings performance and current financial position of a company. Management accounting, also known as managerial accounting, is the process of analyzing information about a company’s finances, interpreting it and using it to make decisions about the business.